Ohio Real Property Conveyance Fee Statement: Don't Forget the Personal Property!

- Steve Nowak

- Feb 21, 2017

- 4 min read

Include the Value of Personal Property on the Conveyance Fee Statement

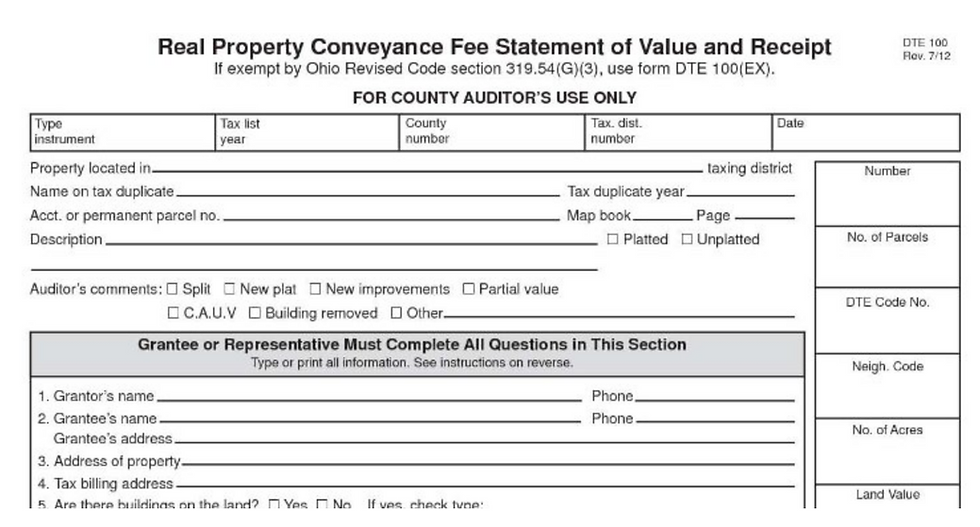

In Ohio, the Real Property Conveyance Fee Statement must be submitted to the County Recorder to get a deed recorded. If you are buying real estate in Ohio, then do yourself (and me) a favor and fill it out accurately. Pay special attention to Section 7 regarding the total consideration paid for the real property.

With shrinking budgets and lower state level contributions, School Boards look for real estate sales with transfer prices above the assessor's valuation. Once the sales are identified, the School Board file tax valuation increase complaints. This is much more prevalent with commercial real estate.

The School Board's Burden of Proof in Real Estate Tax Appeal

Since the School Boards are not involved in the sale transaction, they look to public records to substantiate their case for the increased value (and increased tax payments). In Cuyahoga County, the Fiscal Officer is going one step further and requesting that a Sale Verification Questionnaire be completed.

Under Ohio law, the School Board can prevail if they present a deed and conveyance fee statement. In Cuyahoga County, the addition of the Sale Verification Questionnaire makes the School Board's job that much easier. These documents are easily obtainable public records. At the very least, the School Board’s production of these very basic documents creates a legal presumption that the dollar amount set forth on the Conveyance Fee Statement or deed is correct.

The problem is that—in my experience—the buyer many times fails to recognize the name/signature of the person who signed the Conveyance Fee Statement. That came be a big problem for the buyer. Sometimes, it is a settlement/closing agent that completes the form and signs it. Of course, the settlement agent is not aware of the nuances of the transaction.

The fact is that when one person (or company) purchases real estate, that person often times purchases more than just real estate. Your real property taxes are based on the value of the real estate only. So, if the sale included the transfer of an on-going business concern, goodwill or personal property (FF&E), then the buyer needs to identify these items and accurately determine/estimate the value of these non-real estate items.

And, critically, the value of the non-real estate items needs to be included in the language of the purchase agreement. The value of the non-real estate items also need to be properly identified on the Real Property Conveyance Fee—there’s a line that asks for the value at line 7(e): “Portion, if any, of total consideration paid for items other than real property.” If a buyer fails to do both of these things, the buyer faces a formidable challenge in trying to reduce the recorded sale price to account for the value of the non-real estate items.

If the value of non-real estate items comes up for the first time in a valuation hearing at the Board of Revision after the School Board filed an increase valuation complaint, the buyer/owner is already behind the eight ball.

Buyers Need a Detailed and Accurate Allocation of Purchase Price that Represents the Value of Personal Property

To do so, the buyer needs to provide a complete and accurate list of the non-real estate items that came with the purchase price. The value allocated to these items needs to be calculated or estimated in an objective, systematic manner that will make sense and be convincing to (in Ohio) the Board of Revision and Board of Tax Appeals.

Be Accurate and Work With the Seller and Expert if Appropriate

Don’t pull a number out of the air! Consider obtaining an independent opinion of value. Depending on the size of the property, the extent of the non real estate items, and perceived value, this step is well worth the money. Finally, negotiate the allocation with the seller and include the itemized and agreed-upon values in the sale documents. Include any supporting or corroborating information supporting the calculations as exhibits to the sale documents. And, for goodness sake, include the value of the non real estate items on the Real Property Conveyance Fee form. It will save you money.

Copyright © 2016 by Stephen M. Nowak

Disclaimer: The post is intended to convey general information only and not to provide legal advice or opinions. The contents of this post, and the posting and viewing of the information on this website should not be construed as, and should not be relied upon for, legal or tax advice in any particular circumstance or fact situation. This post is intended to inform the general public of its legal rights. No formal legal action should be taken in reliance on the information contained in this post and Steve Nowak and Steve Nowak Law, LLC disclaims all liability in respect to actions taken or not taken based on any or all of the contents of this post to the fullest extent permitted by law. An attorney should be contacted for advice on specific property or specific property tax appeal.

Comments